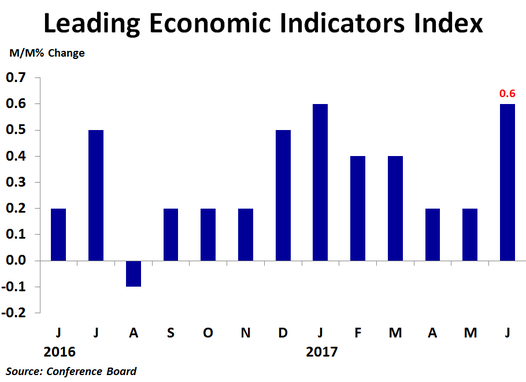

The leading economic indicators index rose 0.6% in June from the prior month following a downwardly revised 0.2% increase in May. The increase was better than the consensus forecast of a 0.4% rise. Compared to a year ago, the index was up 4.0%, far higher than May’s 2.7% pace. Over the six month period ending in June, the index was up 2.5%, up slightly from the 2.3% rate of growth in the six months ending in May.

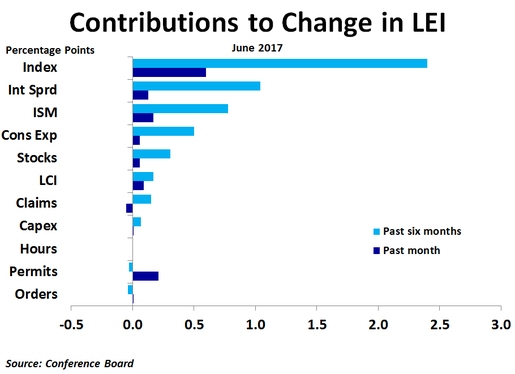

Building permits led the way in June, contributing 0.21 percentage points to the growth in the overall index, as building permits rebounded from a very weak May to post a strong 1.254 million unit annualized reading for June. The ISM new orders index came in second, contributing 0.17 percentage points as the index rose to 63.5 in June from 59.5 in May. The interest rate spread between the 10-year Treasury yield and the Federal Funds rate was next, contributing 0.13 percentage points to the growth in the index. Although this was the smallest contribution from this component since July as the spread has narrowed, this component has still contributed the most to the rise in the index over the past six months. Consumer expectations for business conditions contributed just 0.06 percentage points, the smallest contribution for this component since November, as consumers have become more concerned that Trump’s pro-growth policies may not come to fruition as soon as previously thought, if at all. The contribution from the stock market held steady at 0.06 percentage points as the market rose slightly in June. For the fifth month in a row, core capital goods orders contributed virtually nothing in June.

The only negative contribution came from initial jobless claims, as average weekly claims rose to 244K in June from 240K in May.

The only negative contribution came from initial jobless claims, as average weekly claims rose to 244K in June from 240K in May.

Although the interest rate spread is often among the largest contributors, its contribution has been trending slightly lower over the last few months as the Federal Reserve has been gradually raising the Federal Funds rate while the 10-year Treasury yield has come down as investors’ initial optimism about the new administration’s economic policies has been followed by some doubt about the chances for successful implementation.

Given slowing inflation, weak wage growth and signs of a possible top in housing, the Fed’s June rate hike appears a bit misplaced. However, the LEI is suggesting growth should pick up soon. It remains to be seen if inflation, and interest rates, follow suit.

Given slowing inflation, weak wage growth and signs of a possible top in housing, the Fed’s June rate hike appears a bit misplaced. However, the LEI is suggesting growth should pick up soon. It remains to be seen if inflation, and interest rates, follow suit.

RSS Feed

RSS Feed