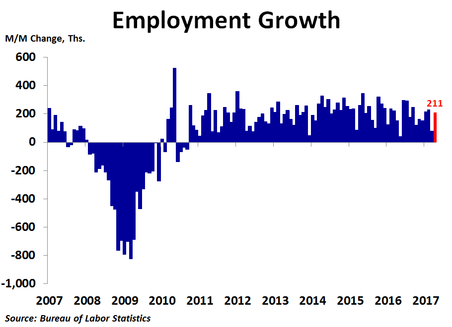

Job growth rebounded in April as the economy generated 211K new jobs, up significantly from the 79K increase in February, and much better than the 185K consensus forecast. Revisions showed 13K more jobs were created in February and 19K fewer in March than previously reported. The rate of job growth inched up to 1.6% year-over-year.

Leading the way in April was a strong 55K increase in leisure and hospitality services, half of which came from food services and drinking places. However, this came after a very weak March for the sector. Professional and business services were next, adding 39K new jobs. Healthcare services saw a 37K increase in staff, though again this followed the weakest month since December 2013. Financial activities had a decent month, adding 19K new jobs after dismal readings in February and March. Following a scant 2K rise in March, government payrolls rose by 17K, driven exclusively by local government. Mining and logging had another good month, putting 10K more people to work, bringing the running six month total increase to 45K. This is very good news as these are high paying jobs. Importantly, retail trade added 6K jobs, the first increase in three months after losing 56K jobs during February and March.

The only real downside in the report was a 7K decline in information services employment, the seventh straight decline and the sector’s worst slump since the recession.

The 132K difference in job growth in April versus March was largely due to strong hiring in leisure and hospitality services and sharp rebounds in retail trade and healthcare.

More good news was a decline in the unemployment rate from 4.5% to 4.4% as the 156K gain in household employment far outpaced the small 12K increase in the labor force, meaning the increase in the labor force was fully absorbed, while 144K people who were already in the labor force, but were not previously working, also found new jobs.

The only real downside in the report was a 7K decline in information services employment, the seventh straight decline and the sector’s worst slump since the recession.

The 132K difference in job growth in April versus March was largely due to strong hiring in leisure and hospitality services and sharp rebounds in retail trade and healthcare.

More good news was a decline in the unemployment rate from 4.5% to 4.4% as the 156K gain in household employment far outpaced the small 12K increase in the labor force, meaning the increase in the labor force was fully absorbed, while 144K people who were already in the labor force, but were not previously working, also found new jobs.

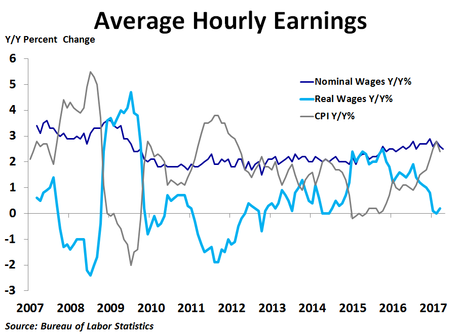

Average hourly earnings rose 0.3% and were up 2.5% from a year ago, down a bit from the 2.9% pace back in December. With inflation moving up recently, real wage growth has cratered and was virtually flat in March.

Very weak GDP growth in the first quarter and slowing job growth and inflation in March led the Fed to hold rates steady on Wednesday. Even so, the Fed believes the recent weakness will likely not last. Today’s job report has bumped up the odds of a rate hike in June, but, as always, inflation will be key.

Very weak GDP growth in the first quarter and slowing job growth and inflation in March led the Fed to hold rates steady on Wednesday. Even so, the Fed believes the recent weakness will likely not last. Today’s job report has bumped up the odds of a rate hike in June, but, as always, inflation will be key.

RSS Feed

RSS Feed