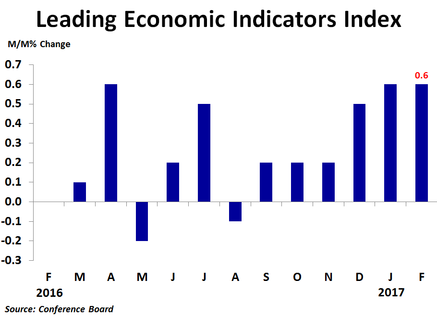

The leading economic indicators index rose 0.6% in February from the prior month following a similar 0.6% increase in January. The increase was better than the 0.4% consensus forecast. Compared to a year ago, the index was up a solid 2.5%, an improvement over January’s 1.9% pace. Over the six month period ending in February, the index was up 2.3% after growing just 1.6% in the six months to January.

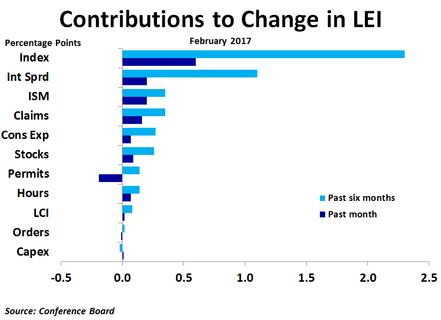

The big story in today’s report was the large negative contribution from building permits, which subtracted 0.19 percentage points from the overall index and was the only negative contribution. Building permits slid to 1.21 million in February from January’s 1.29 million, although housing starts rose sharply.

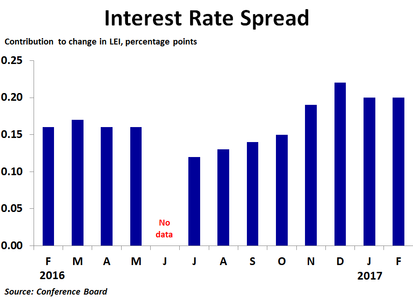

The biggest positive contribution came from the interest rate spread between the 10-year Treasury yield and the Federal Funds rate, which contributed 0.20 percentage points to the index. Although the interest rate spread is often among the largest contributors, its contribution has been trending higher over the last several months as investors have been selling bonds in anticipation of higher inflation and stronger economic growth supported by lower taxes, fewer regulations and heavy infrastructure spending under President Trump. The ISM new orders index also contributed 0.20 percentage points as the recent strength in manufacturing survey data continued. The ISM contribution to the overall index has been noticeably stronger in the last three months. Still, the contribution from actual non-defense orders excluding aircraft has been fairly weak during this same period. Initial jobless claims contributed 0.16 percentage points as claims averaged 237K per week in February, down from January’s 248K. A further rise in the stock market contributed 0.09 percentage points. The same indicators that contributed the most over the past month have also contributed the most to the index over the past six months.

The biggest positive contribution came from the interest rate spread between the 10-year Treasury yield and the Federal Funds rate, which contributed 0.20 percentage points to the index. Although the interest rate spread is often among the largest contributors, its contribution has been trending higher over the last several months as investors have been selling bonds in anticipation of higher inflation and stronger economic growth supported by lower taxes, fewer regulations and heavy infrastructure spending under President Trump. The ISM new orders index also contributed 0.20 percentage points as the recent strength in manufacturing survey data continued. The ISM contribution to the overall index has been noticeably stronger in the last three months. Still, the contribution from actual non-defense orders excluding aircraft has been fairly weak during this same period. Initial jobless claims contributed 0.16 percentage points as claims averaged 237K per week in February, down from January’s 248K. A further rise in the stock market contributed 0.09 percentage points. The same indicators that contributed the most over the past month have also contributed the most to the index over the past six months.

Over the past year, only the leading credit index has seen deterioration, while all other components have been improving. The strongest contributor recently has been the widening interest rate spread, which should help to boost lending as banks see wider interest margins on their loan products. This should help to lift overall economic activity. Still, it depends on how much demand there will be for loans. With manufacturing improving and job growth strong, the economy should find firmer ground soon; should being the operative word as productivity remains woefully weak.

RSS Feed

RSS Feed