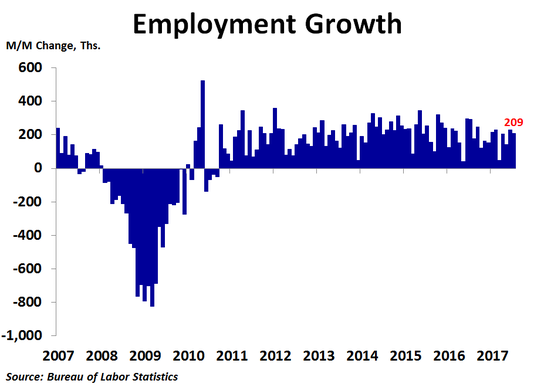

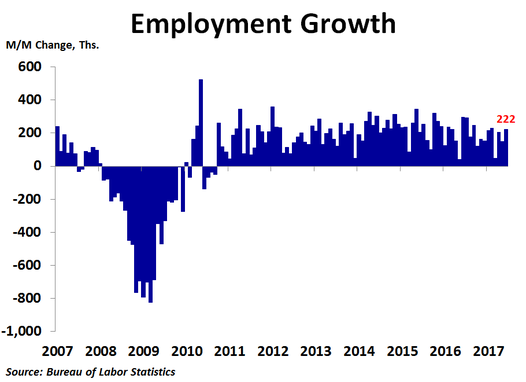

Job growth was strong again in July as the economy added 209K new jobs, a little less than June’s 231K increase but much higher than the 178K consensus forecast. Revisions were negligible. The year-ago rate of job growth slipped to 1.5%, the lowest since May 2011.

Leisure and hospitality services led the way in July, putting 62K more people to work, mostly in food services and drinking places. Education and healthcare services added 54K new positions, with 45K of them coming from healthcare. Professional and business services also had a strong month as 49K people found new jobs, 15K of which were in temporary help services. Manufacturing had a decent month as 16K more people were hired. Wholesale trade added 6K more people to staff. The construction industry had a fairly weak month as only 6K new jobs were created. In the last five months construction has only added 28K new jobs amid a slowdown in home building. Financial services also had a weak month, with only 6K new positions being filled. Information services added 4K new people to the payrolls, the second straight gain following eight months of losses totaling 62K jobs. This is good news as these are among the highest paid jobs in the economy. Government added just 4K new jobs following a surge in June. Following four months of losses, the retail industry has created 3K new jobs in the past two months; not much, but at least jobs are being created. Following eight straight months of gains, mining and logging employment was flat in July.

The only industry that lost jobs in July was utilities, and even that was a mild decline of just 900 positions. The fact that only one industry lost jobs in July goes to show how strong today’s report really is.

The only industry that lost jobs in July was utilities, and even that was a mild decline of just 900 positions. The fact that only one industry lost jobs in July goes to show how strong today’s report really is.

The 22K decline in job growth in July versus June was largely due to much less hiring in government and fewer jobs being created in other services and healthcare.

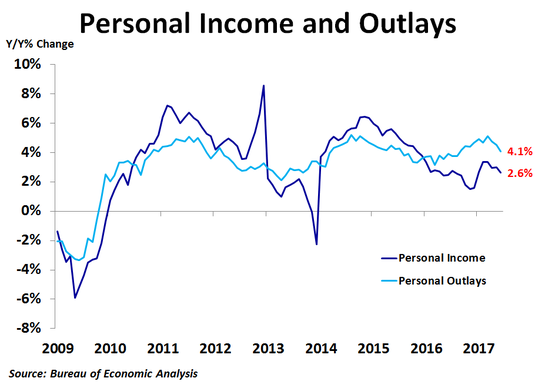

Even though 349K people entered the labor force in July, the unemployment rate fell from 4.4% to 4.3% as 345K of them found jobs, a remarkable 99% success rate!

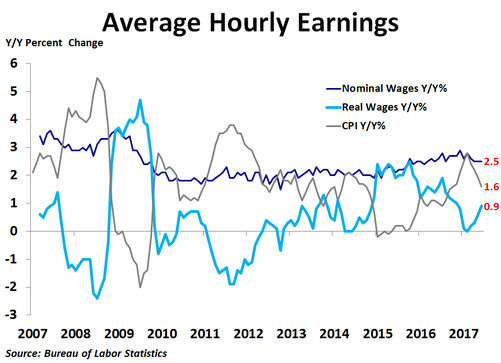

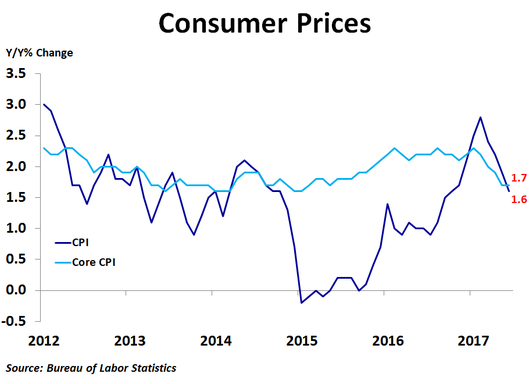

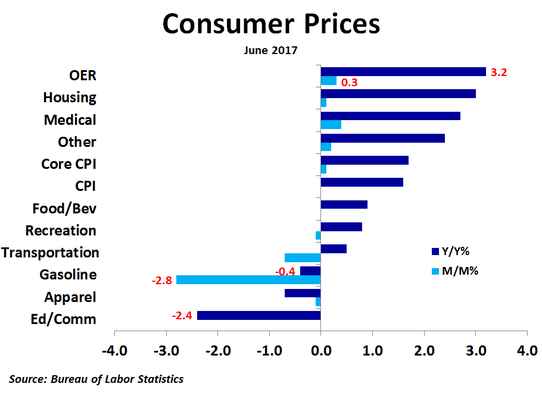

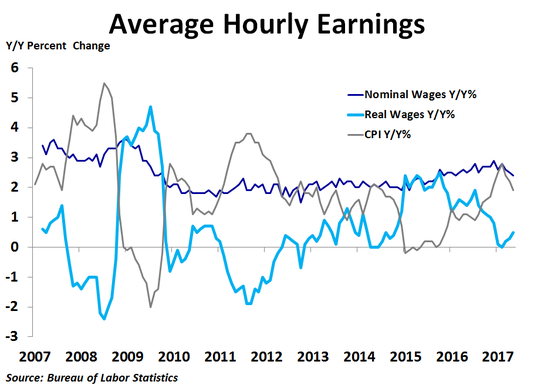

Average hourly earnings rose 0.3% and were up 2.5% from a year ago for the fourth straight month. With inflation cooling recently, real wage growth has rebounded slightly but remains very weak at just 0.9%.

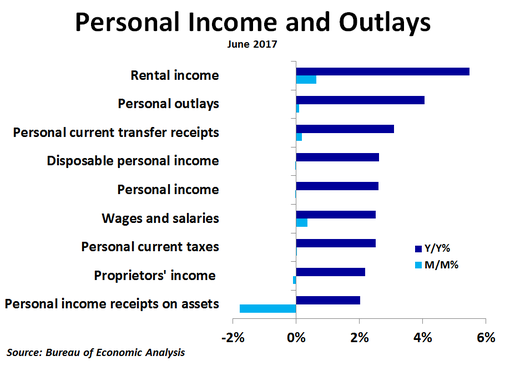

Today’s report may give the hawks more incentive to push for another Fed rate hike soon. Even so, inflation remains well below the Fed’s target, so a rate hike is not necessary.

Even though 349K people entered the labor force in July, the unemployment rate fell from 4.4% to 4.3% as 345K of them found jobs, a remarkable 99% success rate!

Average hourly earnings rose 0.3% and were up 2.5% from a year ago for the fourth straight month. With inflation cooling recently, real wage growth has rebounded slightly but remains very weak at just 0.9%.

Today’s report may give the hawks more incentive to push for another Fed rate hike soon. Even so, inflation remains well below the Fed’s target, so a rate hike is not necessary.

RSS Feed

RSS Feed